Welcome to our April 2025 Investment Summary, where we blend a bit of springtime optimism with the careful strategy that drives long-term growth. As we step into Quarter 2, the markets are beginning to bloom, much like the season itself, bringing new opportunities and challenges. While April Fools’ Day might have had us questioning what’s real and what’s not, we’re taking a grounded approach to the current economic landscape, focusing on the data and trends that matter most. Whether you’re navigating the uncertainties or positioning for growth, we’re here to help you make sense of it all in a market that’s anything but foolproof.

In this month’s investment summary for April, our Chief Investment Officer, Jeff Brummette, reflects on March and provides insights into the key market movements, emerging opportunities, and an outlook for the months ahead as we start the second quarter of 2025.

_______

President Donald Trump’s tariff rhetoric turned into reality for markets in March as a series of significant tariffs were unveiled: 25% on goods from Canada and Mexico, along with 25% tariffs on foreign-made automobiles. Further tariff announcements are expected on April 2, which Trump has designated ‘Liberation Day‘. Presumably he is liberating the USA from the tyranny of trade deficits. In response, the rest of the world has vowed retaliation.

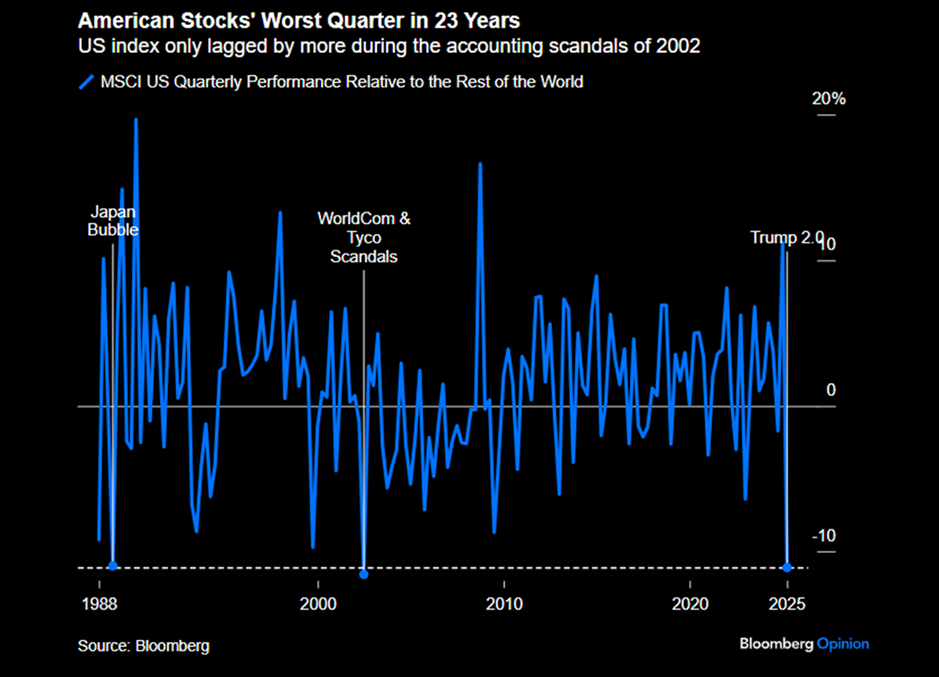

American Stocks’ Worst Quarter in 23 Years

Source: Bloomberg

None of this bodes well for financial markets. All major equity markets declined in March following the tariff announcements.

Equity Markets

Source: Bloomberg

Fixed income offered no relief, as longer-term yields rose in the UK and Eurozone, while remaining unchanged in the U.S. In alternative assets, Bitcoin failed to make a positive contribution, but gold had a very strong month, and oil also posted gains despite the economic threat that is likely to come with tariffs.

Fixed Income Markets

Source: Bloomberg

Alternative Investments Markets

Source: Bloomberg

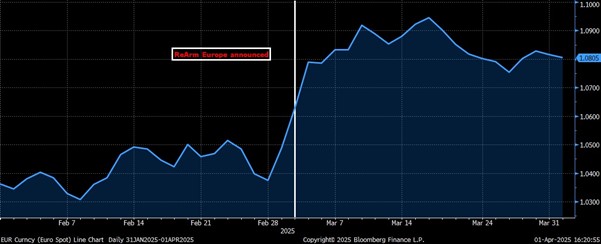

Looking at the full quarter, it is notable that the Eurozone, China, and the UK all had a strong start to the year, despite the declines in U.S. markets. Europe responded to Trump’s abandonment of Ukraine and near embrace of Putin by committing to significant increases in defence spending. EU Commission President Ursula von der Leyen paraphrased Mario Draghi and stated, “Europe would do whatever it takes” to boost defence spending. In her words “I will inform the member states through a letter about the re-arm Europe plan. Europe is ready to assume its responsibilities. ReArm Europe could mobilise close to EUR €800 billion for a safe and resilient Europe. We will continue working closely with our partners in NATO. This is a moment for Europe. And we are ready to step up.”

The EU approved a €150 billion lending facility for defence spending and agreed to exclude defence spending from the calculations for measuring fiscal deficits. This move could free up €650 billion more to spend on defence. Not to be outdone, Germany revised its fiscal rules to exclude defence spending above 1% of GDP from their deficit calculations and also announced a €500 billion ten-year infrastructure spending program.

European equity markets and the Euro responded positively to these measures, reflecting investor confidence in the region’s economic and security commitments.

EUR/USD

Source: Bloomberg Finance L.P.

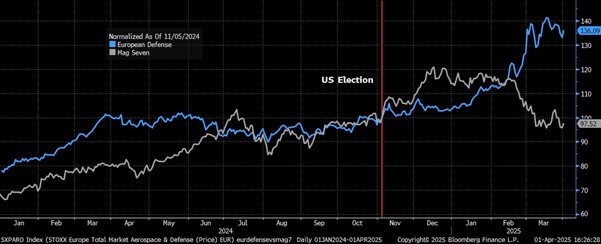

More importantly, the response from European defence firms was even stronger, driving much of the quarter’s gains in European equity indices. This marked a stark contrast with the so-called “Magnificent Seven” tech stocks, highlighting a major shift in market leadership.

Euro Stoxx 600 Defence vs. Magnificent Seven

Source: Bloomberg Finance L.P.

Chinese technology remained resilient in March as markets continued to digest the significance of the DeepSeek announcement.

DeepSeek News vs. Alibaba vs. Magnificent Seven

Source: Bloomberg Finance L.P.

Monetary policy meetings were held by the Bank of England (“BoE”), the European Central Bank (“ECB”), the U.S. Federal Reserve (“Fed”), and the Bank of Japan (“BoJ”) during March. While the BoE, Fed, and the BoJ kept rates on hold, the ECB cut interest rates by 25 basis points. All four central banks expressed confidence that inflation would meet their respective 2.0% targets. However, while the ECB sounded as though they were finished cutting rates, the BoE and the Fed both suggested more rate cuts could occur if inflation fell further.

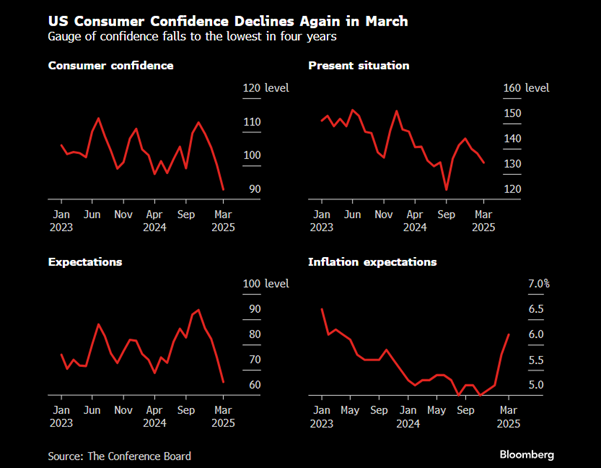

A common theme across all four institutions was the high degree of uncertainty around their forecasts, largely due to the prospects of significant tariffs on trade. This uncertainty is also weighing on U.S. businesses and households, with confidence surveys dropping sharply and inflation expectations are rising. This is not a good mix for financial markets or for spending. Given this backdrop, it’s perhaps no surprise that the price of gold keeps rising.

Gold $/oz

Source: Bloomberg Finance L.P.

Trump’s pledge to cut wasteful government spending via the actions of Elon Musk’s Department of Government Efficiency (DOGE), has resulted in chaotic firings of federal workers and the cancellations of a great many consulting contracts with private firms that support various federal agencies. This is certainly weighing on confidence. There are suggestions that staff cuts at the IRS may result in delays in tax refunds being processed. It is not helping that a variety of Trump officials are suggesting that a recession is possible and may be the price that needs to be paid to transition into the “wonderful new economy” Trump is promising.

US Consumer Confidence Declines Again in March

Source: The Conference Board via Bloomberg

President Trump remains indifferent to concerns that tariffs will drive up prices. He views tariffs as a way to bring manufacturing jobs back to the USA and has vowed even greater tariffs on countries that resist or put counter tariffs on U.S. exports.

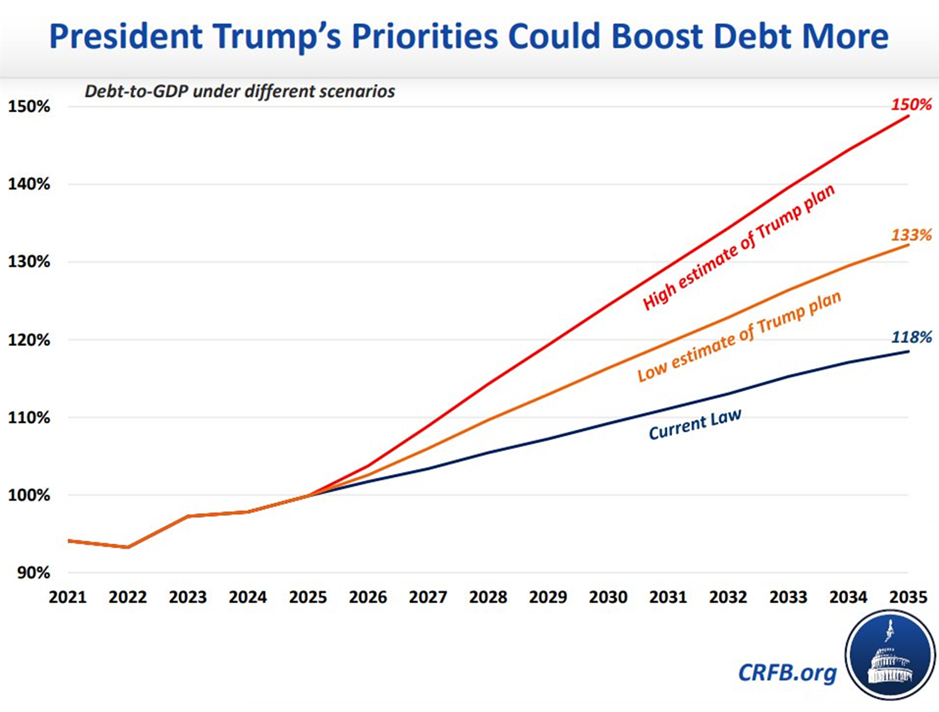

Meanwhile, tax cuts are promised as a stimulus to help boost the economy, but with the deficit already so large, there is little room to expand it further without triggering a negative reaction from financial markets.

President Trump’s Priorities Could Boost Debt More

Source: Committee for a Responsible Federal Budget (CRFB.org)

Given these developments, we remain comfortable holding an underweight position in the U.S. Europe appears more focused and united than it has been in some time, and we expect their move to spend more on defence is a new long term secular tailwind for Europe.

Meanwhile, China continues to push for economic stimulus, particularly by encouraging consumption, while Trump’s policies are making it increasingly difficult to conduct business in the U.S.

In response to the risk of an economic slowdown, we have been increasing the duration of our fixed income holdings, positioning for a more challenging growth environment ahead.

_______

Hear more from the Oakglen experts

Our investment team continue to provide interesting and informative content to help keep you in the loop on recent global news and market trends. See below for some key highlights from around the world which some of the investment management team have recently covered:

Read more:

- The Global Automotive Sector: Losing Grip of the Wheel?

William Lamond, Investment Director

- March 2025 Investment Summary

Jeff Brummette, Chief Investment Officer

- Central Bank Update: February 2025

Jeff Brummette, Chief Investment Officer

You can read other articles from the team on our News & Insights page.

Sign up below to receive similar content directly into your inbox.

Want to become an Oakglen client?

Get in touch with one of our wealth team via the Contact Us page to hear more about our products and services, and how suitable they are for you and your personal circumstances.